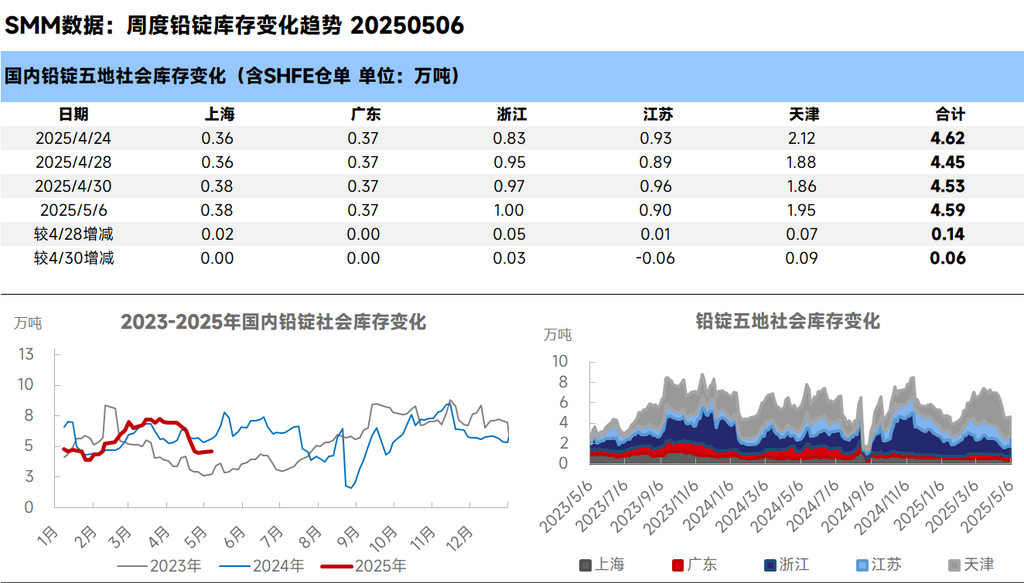

SMM News on May 6: According to SMM, as of May 6, the total social inventory of lead ingots in five regions tracked by SMM reached 45,900 mt, an increase of 1,400 mt from April 28 and over 600 mt from April 30.

Following the Labour Day holiday, enterprises along the lead industry chain, both upstream and downstream, gradually resumed trading. On the first trading day after the holiday, lead prices weakened, with downstream enterprises adopting a wait-and-see attitude. Trading in the spot market was relatively sluggish, and the social inventory of lead ingots in warehouses also increased compared to pre-holiday levels. During the Labour Day holiday, lead-acid battery enterprises had longer holidays than lead smelters, creating a natural gap in lead consumption. As a result, smelters generally saw an increase in inventory. Additionally, with the SHFE lead 2505 contract expected to enter delivery next week, there is a possibility of transferring delivery brands to delivery warehouses. It is anticipated that the social inventory of lead ingots will continue to rise. Furthermore, lead prices have diverged from the trend of raw material prices. In particular, the price of scrap batteries remains high and has even risen against the trend, exacerbating losses for secondary lead enterprises. Close attention should be paid to the impact of production trends in secondary lead enterprises on inventory in the near future.